Irish Life answers some frequently asked questions for participating employers in the EMPOWER Master Trust

What is a master trust?

Before understanding what a master trust is, it’s important firstly to know what a trust is. Company pension plans are normally set up under a trust, which is designed to protect members by separating the assets of the pension plan from those of the company. A trust is a legal instrument and provides an extra layer of security and separation to help keep plan members’ pension savings safe. A master trust is basically a ‘master’ pension plan, which allows multiple company plans to participate under one large trust. Who is trustee of the EMPOWER Master Trust?

Law Debenture Ireland Master Trust Trustee (Ireland) DAC (LawDeb Ireland DAC) is trustee of the EMPOWER Master Trust. LawDeb Ireland DAC is completely independent of Irish Life, which is quite a unique feature in the Irish master trust market. To find out more head over to our Meet the Trustee section. Where can I (or my employees) find out more about Auto-Enrolment (AE)?

The aim of an Auto Enrolment (AE) system is to make the decision easier for workers to save for a pension. It also makes it easier for employers to offer colleagues a workplace pension. The Government is still working on the final legislation, which is likely to dictate the implementation date. Irish Life is a strong advocate for auto enrolment. We share some of the AE journey here. When are my plan contributions due?

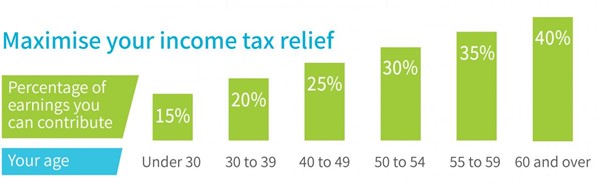

All contributions deducted from employees and due from employers must be paid to the pension scheme within 21 days of the end of the month in which they were deducted or became due. It is your responsibility as an employer to ensure that you arrange for the transmission of this report and payment of contributions within the prescribed timeframe. What are the tax relief limits for my employees?

All contributions deducted from employees and due from employers must be paid to the pension scheme within 21 days of the end of the month in which they were deducted or became due. It is your responsibility as an employer to ensure that you arrange for the transmission of this report and payment of contributions within the prescribed timeframe. Below is an example of how tax relief works on a contribution of €100: 40% tax rate Contribution of If a pension plan member wants to increase the value of their pension fund, they can do so by making regular Additional Voluntary Contributions (AVCs) or a once off lump sum contribution. The good news is that they may also get tax relief on these contributions. AVCs are the same as regular pension contributions when it comes to getting tax relief and as such are subject to the same tax relief limits. However, employers may choose not to match AVCs. The table below displays the percentage of an employee’s earnings that may qualify for tax relief when contributing to a pension plan. This includes any compulsory contributions to their plan and any AVCs they might choose to make. Revenue limits are applied to a members’ total earnings, subject to a maximum earnings limit of €115,000. Please note that contributions to an employer pension plan are a percentage of basic salary, rather than total earnings. The earnings limit is subject to review. Can we change how we pay pension contributions?

Yes, you can alter the payment method for your plan’s pension contributions. Head over to our payment methods section to find out more. Can an employee still contribute to the pension plan if they leave the company or move abroad?

Generally, once an employee leaves the company (or group of companies), they can no longer contribute to the company pension plan. However, in some cases, if they are moving to another company or country, but staying within a larger group of companies, they may be able to continue contributing. So, you would need to check your own specific pension plan rules for a definitive answer. How does an employee make an Additional Voluntary Contribution (AVC)?

If the company allows employees to make AVCs, this can be facilitated through your payroll and would be paid with the standard monthly pension contributions. Alternatively, if an employee decides to make a once-off lump sum payment into their pension before October 31, they may still qualify for a tax relief in respect of the previous year. Click here to find out more. Can an employee choose or amend their own investment funds?

Pension plan members can request to switch funds online within the investment section of the Pension Portal, or by completing this form and sending to us by post or email at the addresses detailed below. Fund Switch via Pension Portal Where can my employees view their fund performance?

The quickest and easiest way for members to view fund performance is via the Pension Portal. Alternatively, full information including fund performance is updated regularly here. Where can my employees learn more about Responsible Investing?

At Irish Life, we’re working hard to make the most of the money your employees have chosen to invest with us. With our Investment Managers, we’re committed to growing the money and doing it responsibly. That means investing more in companies that manage their environmental, social and governance risks in a better way. In fact, Irish Life Investment Managers (ILIM) are currently managing nearly €40 billion* of responsibly managed assets. Also, they’ve been independently recognised as Investment Managers of the Year at the Irish Pension Awards for 6 of the last 8 years**. To find out more and use our Carbon Calculator to help you to discover the real-world impact of your investments, just click here. What happens when an employee leaves the company?

When an employee leaves the company, the employer should notify Irish Life of their date of leaving service and we will send them a Statement of Options as a matter of course. This Statement of Options outlines the various choices they have when it comes to their pension savings in detail, taking into account the scheme rules, their length of time in the scheme, their personal circumstances etc. However, at a high level, members typically have 3 possible options in this situation, and members over 50 also have a 4th potential option: Option 1 Deferment: This option allows members to leave their existing savings in the pension plan until their Normal Retirement Age (NRA). When they leave the company, they cannot pay into the pension anymore, but their savings to date will remain invested for them in the meantime. They will also continue to receive benefit statements each year, they can still access the Pension Portal and they can still make fund switches, if they wish to do so. Option 2 Transfer: Members may be allowed to transfer their pension savings to a new company pension plan. If they are choosing this option, there are a few simple steps in the process to be aware of. Firstly, they will need to check with their new plan trustee(s) to ensure the trustee(s) will facilitate the transfer before choosing this option. If the trustee(s) are happy to facilitate the transfer, the member will then need to provide us with 3 things: 1. contact details for the administrator of the new plan This will allow us to complete a Transfer of Benefits form for them, which then needs to be sent to the administrator of the new plan. If they do not join another company pension plan, they may decide to set up a Personal Retirement Savings Account (PRSA). In certain circumstances, they may be able to transfer the value of their retirement savings into the PRSA (subject to meeting certain requirements). They could also consider taking the value of their retirement savings from the company plan and investing in what is known as a Buy-Out-Bond or a Personal Retirement Bond (PRB). The terms of the PRB will generally follow the pension plan rules. Option 4 **for members over 50 only**: If they are over the age of 50 and have left the company, they may be allowed to withdraw their pension savings early once their plan trustee(s) consents. It’s important to note that a pension plan is designed to continue until they reach Normal Retirement Age (NRA), so withdrawing savings earlier means their pension fund is likely to be lower in value than it would be if they stayed in the plan right up until their NRA. ***Top Tip*** If they do leave the company, they will still have access to the Pension Portal so they can check in with their pension savings anytime they like. They should add a personal email address to their Pension Portal account before they finish up and ensure that their postal address is up to date too. To discuss their options in more detail. Members can email us at happytohelp@irishlife.ie or call 01 7042000. Can an employee transfer previous pension benefits into an Irish life plan?

The rules around transferring benefits from a previous pension plan into an Irish Life plan depend on many factors. To find out more (or to direct your members to find out more) click here. Can an employee access their retirement savings early?

If the employer and the trustee(s) agree, a member may retire early, once they have reached age 50. The individual would be required to leave the employment of the company to access their retirement savings early. However, the pension is designed to provide benefits at their Normal Retirement Age (NRA), so retiring earlier means that their retirement savings may be lower than they might have been at NRA. Who can I contact for more information or if my question isn’t answered above?

If your question isn’t covered above, we’d be delighted to help. So, feel free to reach out and email us at happytohelp@irishlife.ie making sure to quote your scheme number to allow us to respond to you as quickly and helpfully as possible. |

||||||||||||||

Irish Life Health

Welcome to Ireland’s newest health Insurer, Irish Life Health. Bringing fresh options and innovation to the health insurance market.

Irish Life

Irish Life the largest life and pensions group and fund manager in Ireland, employing 2,000 people and servicing one million customers.

Irish Life Investment Managers

Managing assets in excess 39bn, ILIM manages money on behalf of multinational corporations, charities and domestics.