Act today for a better auto-enrolment plan

Ireland's pension landscape is undergoing significant change with the introduction of auto-enrolment pensions (AE), a new retirement savings plan for Ireland's workforce. It aims to make saving for retirement easier and to simplify the process for employers to offer their employees a pension plan. It has the potential to help people maintain a higher standard of living in retirement and is a top priority for Irish Life. We have given expert advice to the Irish Government on AE since the first draft consultation. Our goal is to drive positive, proactive cultural change across Ireland, helping to improve pension participation and retirement outcomes for everyone. Starting 1 January 2026, auto-enrolment pensions will be introduced in Ireland. So, what do employers need to know and how should they prepare? |

|

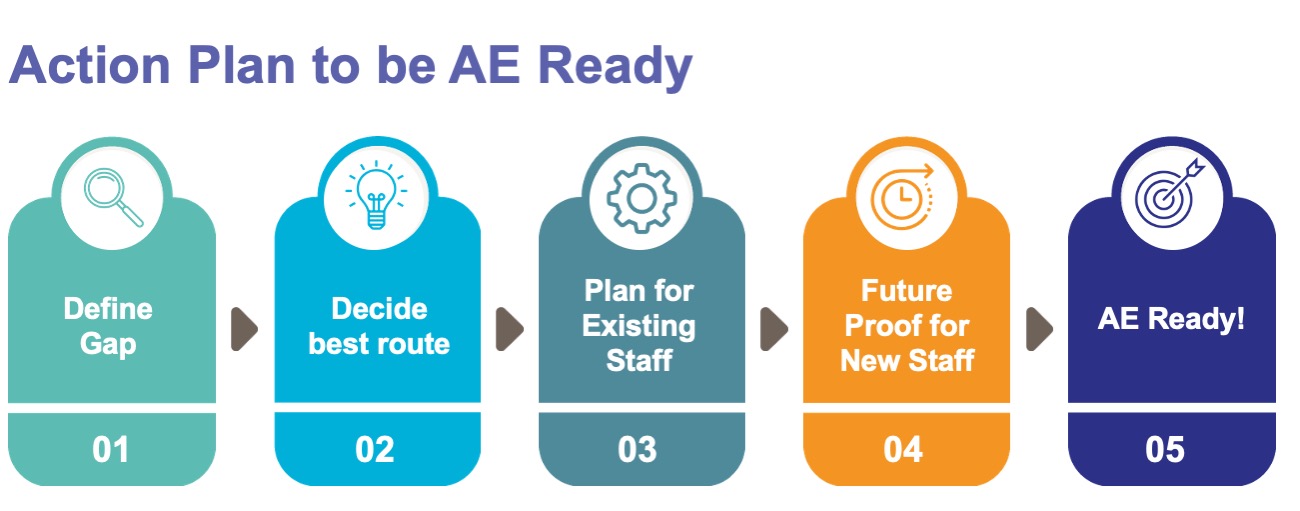

What do employers need to consider?Employers need to prepare for AE as the Government have confirmed a date of 1 January 2026 to the introduction of AE pensions in Ireland with employers needing to be fully compliant by then. This means they will need to set up access to the Government’s AE system by this date for all employees who are not members of any other company pension scheme. That includes those who have opted out of an in-house occupational scheme, those working through a waiting period and temporary staff. The new AE system will exist alongside the current occupational pensions system. This means that employers will be able to use their own occupational pension plan (or a Personal Retirement Savings Account) to meet AE requirements instead of using the central system if the plan meets certain minimum standards. The main initial steps employers need to undertake:

Once this decision had been made there may be several steps to be taken to prepare for AE going live, including reviewing contracts of employment and relevant employment policies as well as potentially amending existing pension arrangements. It is vital that all employers understand the extent to which it might impact them and the immediate and longer-term implications for their business and their employees. We’re here to guide you through the process, speak to one of our pension experts today. |

|

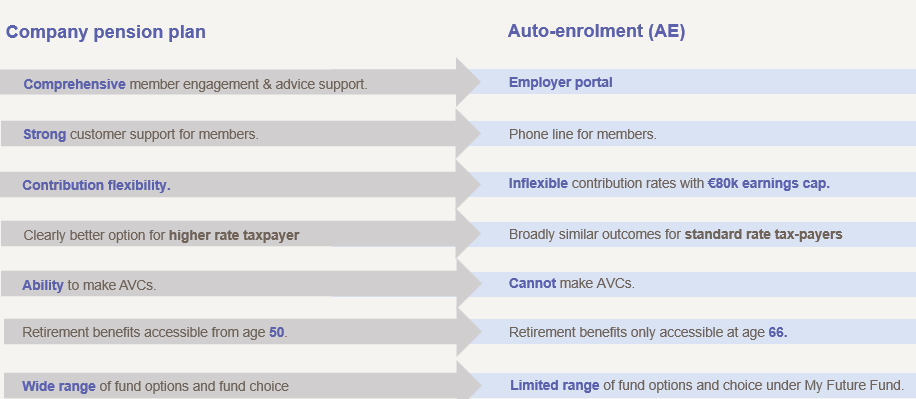

Company pension plan vs Auto-enrolment |

Employer choice and control is a valued part of a company pension plan with employers having the flexibility of choice in who they appoint as their provider, and the type of services delivered within. Whereas the State solution removes any opportunity of choice or control in who provides their company pension plan, and the services delivered. There are a number of differences between a company pension plan and AE and to help you understand these differences in greater detail, we have prepared a comprehensive comparison below: |

|

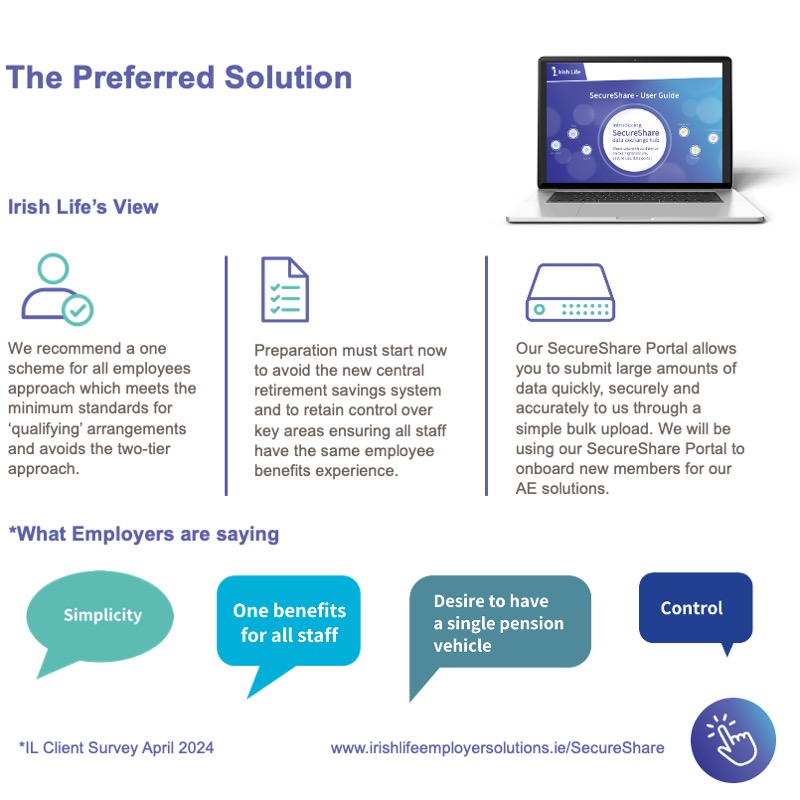

How can Irish Life Employer Solutions help?Irish Life Employer Solutions is the No.1 provider of company benefits for Ireland’s employers making it easier for employers and their workforce to take care of their health and financial wellbeing. We are a trusted partner for Ireland’s corporates and partner with the top 10 Irish employers and 28/30 of the largest FDI employers. Our strong relationships are underpinned by more than 85 years of insight and experience, supported by unrivalled industry knowledge and culture. We work closely with our employers to better understand their needs and provide expertise and insights so we can guide our clients to find the best solution for their organisation and its employees. |

|

Irish Life has created SecureShare, a data sharing portal that allows employers to simply and easily onboard new members. Through SecureShare, employers can submit large amounts of data quickly, securely and accurately.

|

Fast 15 - Podcast Irish Life's new podcast providing expert insights from the Irish Life Employer Solutions team on the latest in pensions, financial wellbeing, health benefits and more. Quick, clear, concise insights for busy decision-makers.

|

Employee Engagement We're here to help support employers with their employee education and communication needs and to help employers explain what AE means for their employees. Our Auto-enrolment Complete Guide is a go-to resource for everything employees need to know. Whether it's a question about how it will work, how it compares to the company pension plan or when it will start, we've got it covered!

|

Frequently Asked Questions:We’ve answered some of the most frequently asked questions for AE below: |

AE is a government retirement savings scheme for employees who are not already actively paying into a pension arrangement through payroll. The aim of AE is to build a culture of saving for retirement in Ireland. The idea is that in retirement, most workers will have their own pension as well as the State Pension, leading to a better retirement income overall.

*800,000+ workers in Ireland, do not have any pension coverage currently and, as a result, will depend on the State Pension as their main source of income in retirement. This means they may see a drastic reduction in their income and living standards. AE will increase both pension coverage and overall pension adequacy by making it easier for employees to access a quality assured retirement savings plan. This system has been successfully implemented in other countries, such as the UK and New Zealand, with strong results in boosting pension participation rates.

It's important to note that many of these workers would be better off joining their company pension plan. However, for those who can’t avail of that option, there is AE.

Eligibility

AE will apply to every private sector worker in Ireland if they are:

- Aged between 23 and 60

- earn more than €20,000 per year from all employment

- and are not currently paying into a company pension or personal pension through payroll.

Enrolment is mandatory for the first 6 months. Members can opt out in months 7 and 8. Those who opt out will be automatically re-enrolled after 2 years.

Employees who do not satisfy the age or earnings thresholds will have the right to opt-in to the AE system, if they choose.

Contributions

- Contributions will be mandatory and need to be made by the employee and employer with a top up from the government.

- Contributions will start at 1.5% of gross earnings, gradually increasing by 1.5% every three years until both the employee and employer are paying to 6% of gross earnings.

- Employer Match: Employers must match employee contributions up to a specified limit.

- State Top-Up: The government will contribute €1 for every €3 saved by the employee, equivalent to a 33% bonus. This means that somebody earning €40,000 will be contributing €600 per year, and their employer and the Government will be adding €800 to their pension fund between them.

- After three years, the contribution increases to 3.0% and the employer and Government contribution increase proportionally. After another three years, it increases to 4.5%, and after 10 years it increases to 6.0% and remains there.

| Years | Employee Contribution | Employer Contribution | Government Contribution |

0-3 | 1.5% | 1.5% | 0.5% |

4-6 | 3% | 3% | 1% |

7-9 | 4.5% | 4.5% | 1.5% |

10+ | 6% | 6% | 2% |

Source: Houses of the Oireachtas (2024). (Automatic Enrolment Retirement Savings System Act, 2024, p. 51)

Note: Employer and Government contributions apply only to salaries up to €80,000. If a person earns more than this, the percentage figure for the employer and Government contributions will be limited to the first €80,000 of gross earnings.

Opt-Out Provision

Enrolment is mandatory for the first 6 months. Members can opt out in months 7 and 8. Those who opt out will be automatically re-enrolled after 2 years.

Investment Options

The National Automatic Enrolment Retirement Savings Authority (NAERSA) will provide employees with a limited range of investment options including a low to medium risk default fund, which will operate on a lifestyle basis, together with three other fund options, classified as low, medium, and high risk.

Investment managers will be appointed to provide funds that will form the investment strategy options for the investment of contributions, including:

- a low-risk strategy

- a medium-risk strategy

- a high-risk strategy

You will be placed in a default strategy to begin with and will have the choice to move to one of the other strategies listed above.

The default strategy will operate on a typical lifecycle basis, which means that the investment risk is decreased as you get closer to retirement. This strategy will see you move from the higher to the medium to the lower risk strategy, based on your age and the number of years remaining until you reach the State Pension age of 66. This strategy takes advantage of high-risk growth in younger years, and the stability of low risk closer to typical retirement age. The default strategy will be structured in a way so that you will not need any financial knowledge or to make choices to get a good retirement income.

Measures will be in place to ensure that these savings, while not guaranteed by the government, will be managed carefully. This includes a rigorous tender process to select investment managers and oversight by the NAERSA Board, the Pensions Authority and the Financial Services and Pensions Ombudsman.

Transferability

Workers can retain their AE pension savings as they change jobs, ensuring flexibility and continuity in their retirement planning.

Administration Charges

Charges will be set nearer the launch date of 1 January 2025, but it is expected there will be:

- A maximum Annual Management charge (AMC) and

- a flat per member charge (to be confirmed).

Key Takeaway |

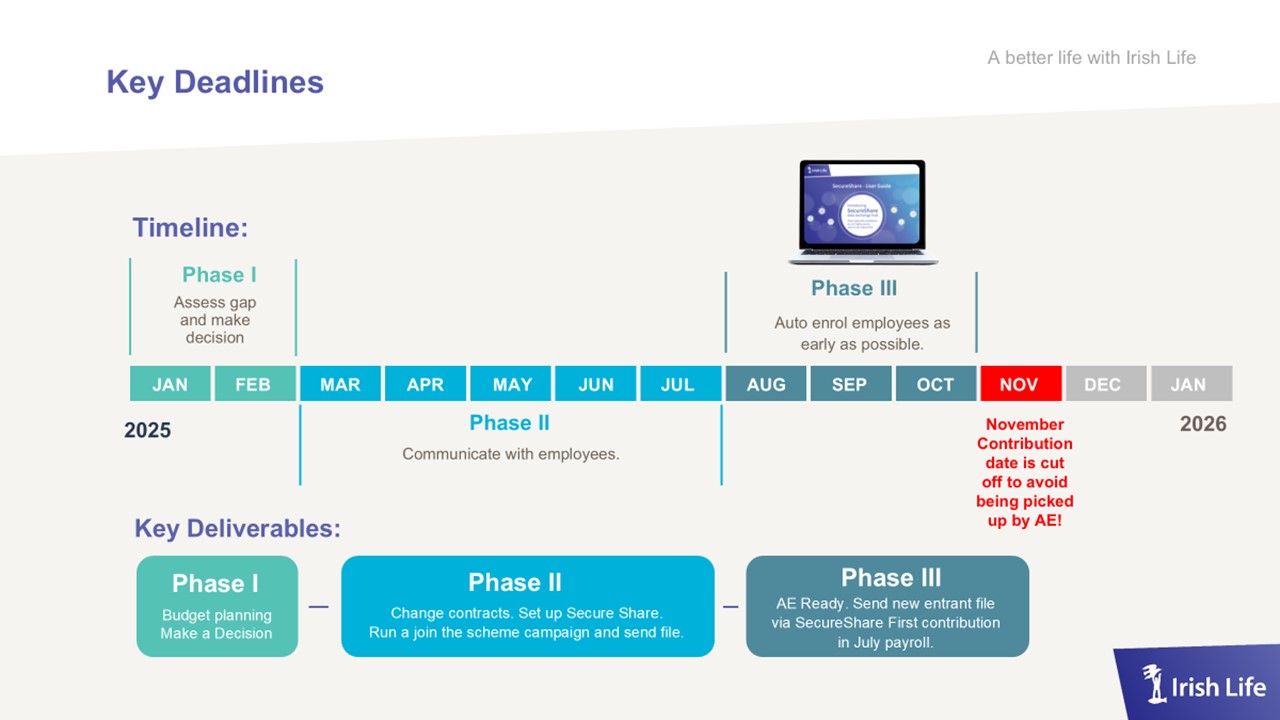

| At Irish Life, we recognise there is unlikely to be a single approach that suits all employers or circumstances. However, our recommended course of action is to have one pension scheme for all employees that meets the minimum standards for ‘qualifying’ arrangements and avoids the two-tier approach. Employers should also note that all new joiners must have their first contributions processed through payroll by the end of November. This process can require several weeks of preparation given standard payroll lead times. For some monthly paid plans, it may mean sign-up must be completed by the end of October to meet the deadline. |

|

By acting today and extending your existing pension plan to all employees now, you ensure a smooth transition, stay in control with one simplified scheme, and support your people beyond the State minimum.

If you would like to prepare for AE with confidence, speak to your Irish Life contact or alternatively, email us at AEready@irishlife.ie today. |

[1] Auto-Enrolment Guide for Employees | Gov.ie – March 2024 [2] Population Ageing and the Public Finances in Ireland | Department of Finance – September 2018 [3] Automatic Enrolment Retirement Savings System Act, 2024 │ Houses of the Oireachtas 2024 |

Irish Life Assurance plc, trading as Irish Life, is regulated by the Central Bank of Ireland. |