|

Women & Pensions: Fast Track to Financial EmpowermentWe all know the benefits of exercise, both physically and mentally, for men and women alike. We feel stronger, more energised and in control. From marathons to triathlons, cycling to CrossFit, and GAA to rugby, let’s face it – people in Ireland But what if I told you women need to exercise more than men to get the same results? Purely because they’re women?! I don’t know any woman – or man – who’d be okay with that concept.

So, Conor finishes up earlier than Laura purely because he’s a man?! Now, obviously this is not how spin classes work, or there would be outrage in every gym in the country! However, the concept does reflect a real-life pension issue in Ireland. |

Let’s be clear – women working until the age of 73, while the men around us retire at 65, is not being posed as a real solution here; that is clearly not the answer. But this significant gap in pension savings between men is a very real concern. Added to that, because women live longer5, that means many of us may need to make ‘less money’ also last longer than the men around us. Which is a very real, very worrying possibility. So, at Irish Life we’re on a mission to raise awareness of this alarming Gender Pension Gap. We are dedicated to financially empowering and supporting the women in Ireland, to take control of your pension so you can make the most out of your hard-earned money. Because all of us – men and women – deserve to enjoy the best possible lifestyle and be as financially secure as we can be when we’re done with work. Keep reading to discover 5 incredibly useful top tips for women so we can all feel confident that we are making the most of our money. But first, a whistlestop tour of what the Gender Pension Gap is and how it might affect your pension. |

What is the Gender Pension Gap?

|

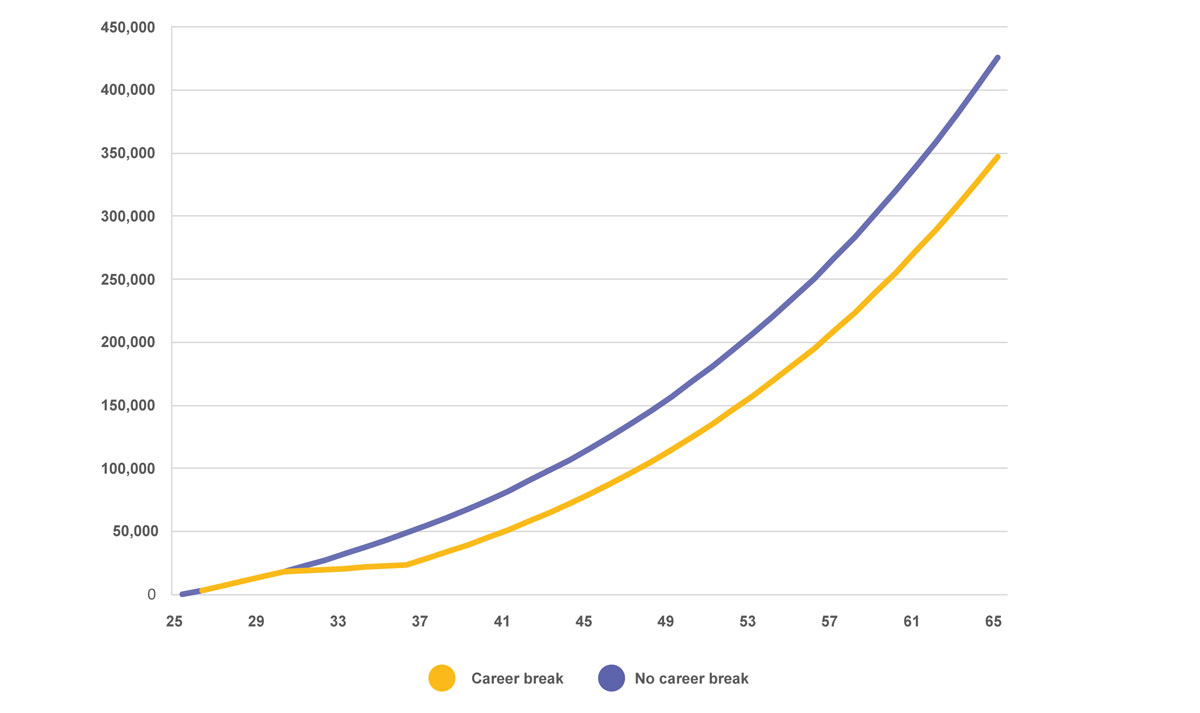

What causes the Gender Pension Gap?The good news is there’s no major difference in the ages that men and women begin saving to a pension, or the % amounts of their salary that they save to their pension7. 1. The gender pay gap 2. Time out of the workforce One thing to be aware of here is this: when we talk about the gender pay gap, we are not examining equal pay or inferring gender pay discrimination or any such thing. And it’s important to know the difference. Let’s explore that for a moment. ‘Equal pay’ refers to whether people are earning the same money for the same work, whereas the ‘Gender Pay Gap’ relates more to the wider gender representation gap, like men having higher paid jobs than women in an organisation for example. Our research found a 22% gender pay gap between men and women. Added to that, Eurostat data also shows that women in Ireland take an average of 6 years out of the workforce, often due to things like maternity leave or working part-time to take care of family. When we combine these two factors, it leads to a 36% gender pension gap. Looking at that gap another way, it means women would need to work 8 more years than men to finish up with the same amount of money in our pension savings. |

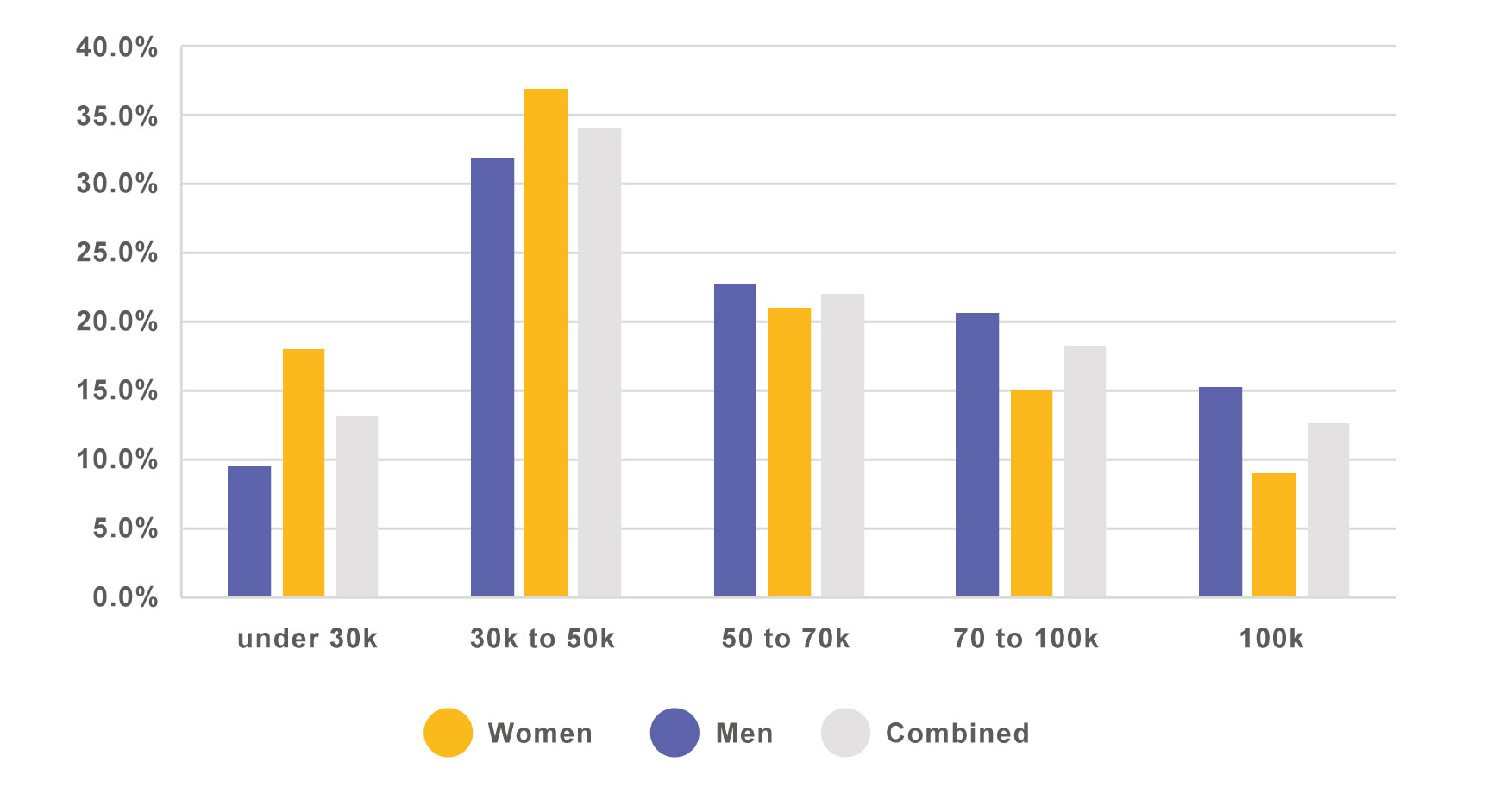

Salary DisparityDid you know that women are 2x more likely to earn less than €30,0008, whereas men are almost 2x more likely to earn more than €100,0009 per year?  Your pension contributions – the money that you save into your pension periodically – are a direct % of your salary. So are the contributions that your employer makes on your behalf. So, although two people may be saving the same % of their salary, the person earning a higher salary is saving more into their pension in monetary terms. Since men are more likely to earn a higher salary (22% higher according to our data), they are also more likely to be saving more – in monetary terms – into their pension than women.  |

|

The data shows that women can expect to live more than 3 years longer than men, which means that your smaller pension pot must also stretch further. So, women are at greater risk of experiencing poverty in later life compared to men11. The phrase ‘we work to live’ comes to mind here because women deserve to retire with as much financial security as possible too, side-by-side with the men in our lives. So, keep reading… here’s what you need to know to understand and optimise your pension, so you can live your best possible life after work on your terms. |

5 Top Tips for Women to Optimise Your Pension: |

1. Be conscious of time.

The key take away here is to save as much as you can from as early in your working life as possible! |

2. Be proactive.

|

In a defined contribution, or workplace pension plan, your employer pays money into your pension savings for you as well, which acts as an amazing top up. Some even offer a tiered structure, where the more money an employee saves, the more they will pay in too, within limits of course. |

4. Review your tax approach.

|

5. Take every opportunity to strengthen your financial literacy. By reading this blog post, you’re taking a great first step! Many women report that they struggle with confidence when it comes to personal finances and pensions14. If you can relate to that, here’s how you can help to get more comfortable in this space: |

|

|

|

| A clear theme from these top tips is that financial empowerment and proactivity are vitally important when it comes to pensions. But you don’t have to do it alone. At Irish Life, we are always here to help. Start by following our top 5 tips to understand how you can make the most of your pension savings, and you’ll never look back. Your future self will thank you! |

|

It’s important to point out that for the purpose of this report, we examine gender purely from a traditional ‘man’ or ‘woman’ perspective. Whilst it’s clear that the whole concept of gender is broader and more fluid than that, the data we use to glean the insights in this report differentiates only by men and women when it comes to gender at this time, though it’s clear that in the future, this debate will evolve. Our defined contribution (DC) group or workplace pension plans serve as our primary data source, with over 130,000 defined contribution plan members included in the data set, though we also gleaned some useful insights from initial outputs of an ongoing research study which Irish Life funded with South East Technological University around young women’s retirement planning in Ireland, which included both independent focus groups and substantial qualitative analysis. |

| Irish Life Assurance plc, trading as Irish Life is regulated by the Central Bank of Ireland. Irish Life Financial Services Ltd is regulated by the Central Bank of Ireland. Irish Life Financial Services is an insurance intermediary tied to Irish Life Assurance for life and pensions and to Irish Life Health dac for health and dental insurance. Irish Life Financial Services Limited is registered in Ireland. Registered Office: Irish Life Centre, Lower Abbey Street, Dublin 1. Registered Number: 489221. |

Sources1: Irish Life, October 2023 3: Irish Life, October 2023 |

Now, let’s imagine this. Conor and Laura are both attending a spin class at their local gym, when 45 minutes into the class, the gym instructor says,

Now, let’s imagine this. Conor and Laura are both attending a spin class at their local gym, when 45 minutes into the class, the gym instructor says,

What does the Gender Pension Gap mean for women?

What does the Gender Pension Gap mean for women?

3. Maximise your employer contributions.

3. Maximise your employer contributions.